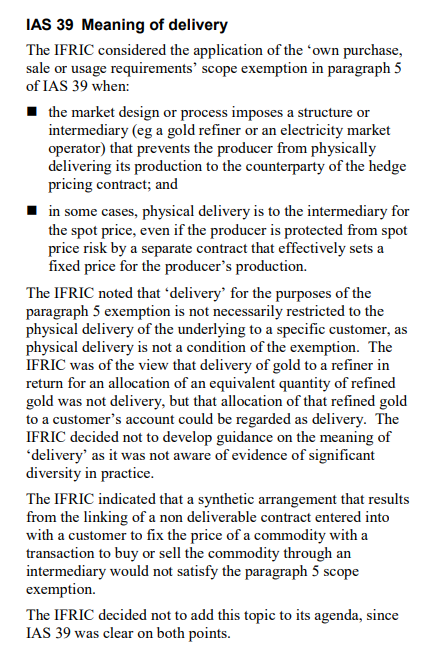

Context

IFRS 9 applies to contracts to buy or sell a non-financial item (such as electricity supply) that can be settled net in cash or another financial instrument, or by exchanging financial instruments as if the contracts were financial instruments unless it meets ‘own use’ purpose.

Analysis

Global corporate clean power procurement reached 62 GW in 2024, surpassing the 46 GW record set in 2023. BNEF said that there is a global push for “more sophisticated corporate clean energy deals” which is “also being driven by regulatory shifts”. This has led to financial reporting challenges because the requirements did not adequately or consistently reflect the economic substance of power purchase agreements, particularly those referencing nature‑dependent electricity such as wind and solar power. In practice, the variable and uncontrollable nature of electricity generation meant that many PPAs failed the ‘own‑use’ exception in IFRS 9 or could not qualify for hedge accounting, even though they were entered into for genuine supply and risk‑management purposes.

The IASB issued amendments to IFRS 9 and IFRS 7 in December 2024 to clarify the application of the own‑use requirements, permit hedge accounting for eligible nature‑dependent electricity contracts with variable volumes, and introduce targeted disclosures in IFRS 7 to improve transparency and comparability for users of financial statements.

The challenge lies in gross pool market, such as Australia and New Zealand.

A gross pool electricity market is a market where all electricity generated and consumed must be traded through a central wholesale pool, with physical dispatch coordinated by a system operator. If a solar farm is developed by a retailer on a client’s property for the client’s use, the electricity is typically exported to the national grid and then supplied back to the client through the grid, with financial settlement through contract-for-difference structure.

Is there a delivery of electricity in gross pool market?

Let’s consider a case-

BCD Ltd enters into a renewable electricity arrangement with a retailer, and the retailer enters into a contract‑for‑difference PPA with the solar developer who develops solar energy in BCD’s land. The retailer supplies electricity to BCD Ltd at a fixed, CPI‑adjusted price. The solar energy produced in BCD’s land flows to the grid (because it’s a gross pool market) and BCD Ltd gets electricity from the grid, with the retailer managing market balancing, excess generation and settlement.

In a gross pool market, there is no direct physical delivery of electricity, and due to its fungible nature and multiple developers delivering to grid, the electricity contract doesn’t normally satisfy delivery definition for ‘own use exemption’ in IFRS 9, unless there is a private wire arrangement, where electricity is supplied directly from a generator to a customer without passing through the grid. Note that the term ‘delivery’ is not defined in the standard, so guidance is taken from a 2005 IFRIC Committee decision relating to what is now paragraph 2.4 of IFRS 9. IFRIC noted that delivery is not limited to physical delivery of the commodity to a specific customer, as physical delivery is not required for the exemption to apply. However, IFRIC also clarified that a synthetic arrangement—where a non‑deliverable contract with a customer is combined with a separate transaction through an intermediary to buy or sell the commodity—would not qualify for the scope exemption.

Type of PPA

Nature of PPA for renewable energy contracts are evolving and can exhibit varying characteristics. XRB, the New Zealand accounting standard board, broadly classifies them into physical PPAs and virtual PPAs.

Virtual PPAs involve the generator and customer buying and selling electricity through the grid at market prices and settling the difference between the market price and the agreed contract price. The purpose of virtual PPAs is to fix the electricity price without requiring physical delivery from the generator to the customer.

The other closely related arrangement is sleeved PPAs. In a sleeved PPA, a retailer acts as an intermediary between the renewable generator and the customer. The retailer typically enters into back‑to‑back contracts with both parties and manages physical delivery and market risks. Under this structure, the generator sells electricity into the grid, while the retailer supplies electricity to the customer as part of its portfolio. The case of Rose Family Estate in New Zealand is a sleeved PPA.

Other factors

The complexity and variety of sleeved PPA structures mean that their treatment as per IFRS 9 may not always be clear. There are other factors that need to be considered, such as:

- Does the buyer have any practical ability to avoid selling it back to the retailer or take benefit of any higher spot price? Is there any speculative intent in the contract?

- Are there Renewable Energy certificates purchased as part of the contract and are these cancelled or retired to offset energy usage from non-renewable sources?

- What is the nature of net settlement clause in the agreement?

- Does the customer purchasing electricity controls the power generator or has significant influence or a joint control?

- If the contract is an executory contract, does it contain any embedded derivatives that need to be separated out?

To conclude, there is no straightforward or definitive answer under the current IFRS 9 guidance and related interpretations as to whether a sleeved PPA meets the own‑use exemption. The assessment is highly dependent on the specific facts and circumstances of each arrangement, including the contractual terms, the role of the intermediary retailer, and how electricity is delivered and financially settled. As a result, sleeved PPAs need to be evaluated on a case‑by‑case basis, with careful consideration of the substance of the contracts and the overall commercial arrangement, rather than relying on form or labels alone.